The Morgan Stanley Swiss Watch Industry Report has finally come as usual. An annual summary on the State of the Swiss Watch Industry compiled by Morgan Stanley and LuxeConsult, a watch industry consulting firm founded by Oliver R. Muller As always, we are here to bring you the most salient parts of this report. If you want to compare with previous years, here are links to the report articles on 2020 and 2021.

In general, the predominant trends hinted at in 2020 – although unreliable – and fully realized in 2021 are confirmed. The premiumization and sales polarization continue to dominate within a market that increases in economic value but decreases in volume.

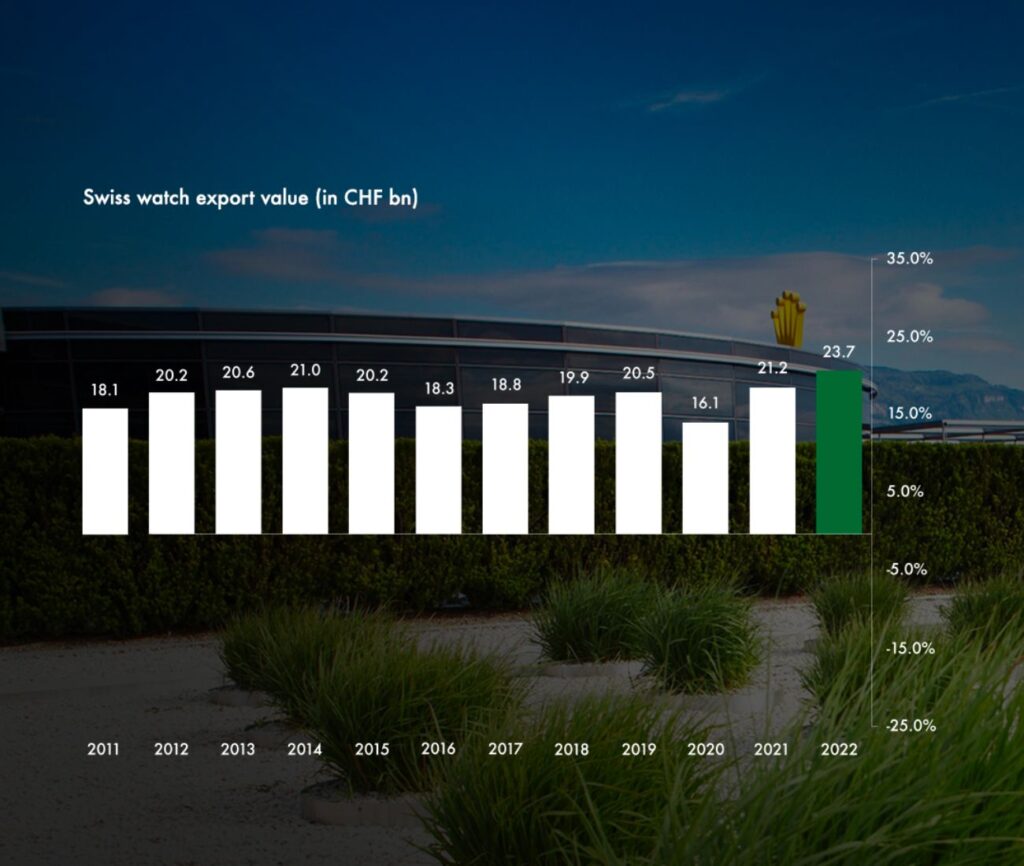

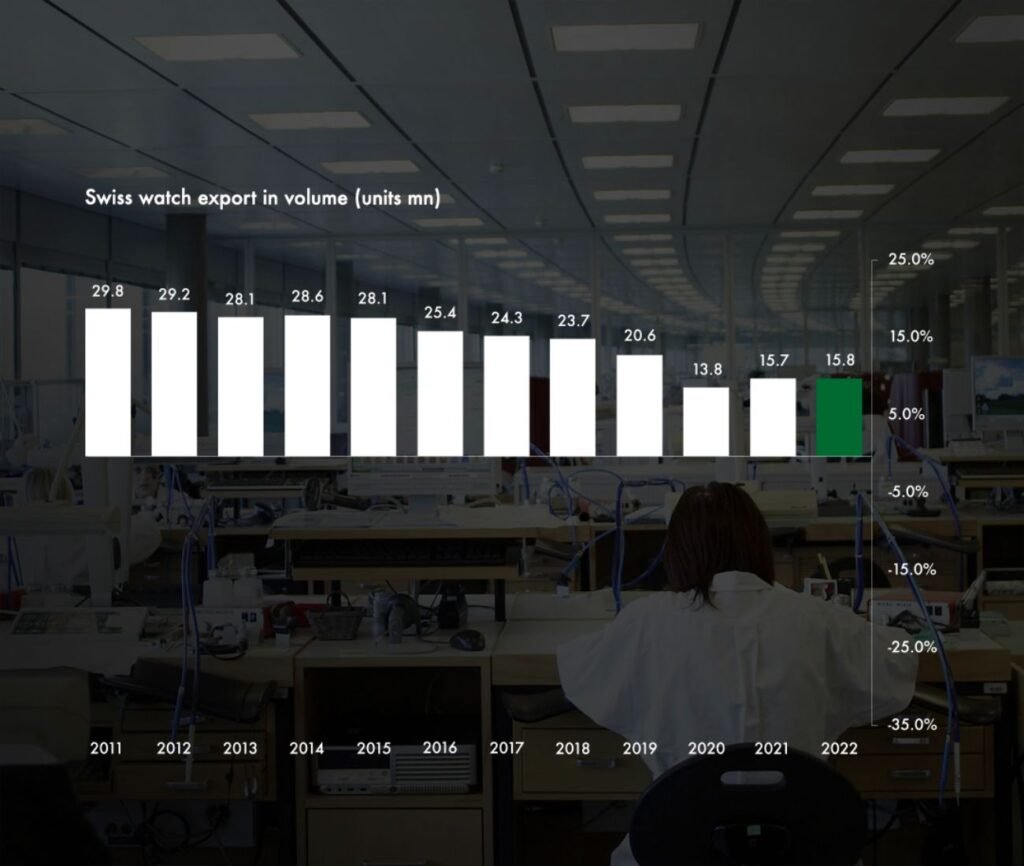

In general, the predominant trends hinted at in 2020 – although unreliable – and fully realized in 2021 are confirmed. The premiumization and sales polarization continue to dominate within a market that increases in economic value but decreases in volume.  The export value of finished watches from the Swiss industry last year reached CHF 23.7 billion. This is up sharply from 2021 (+11.6 percent) but also compared to pre-pandemic levels in 2019 (+9 percent). As for retail sales, Morgan Stanley estimates the value to be around CHF 48 billion. Despite the increase in economic value, it is worth noting that there is no concomitant increase in volume. From 15.7 million watches exported in 2021, we have gone to just 15.8 million (+0.2 percent). This figure testifies even more clearly to the impact of price increases within the industry and also to a certain insensitivity of the target audience to the variant.

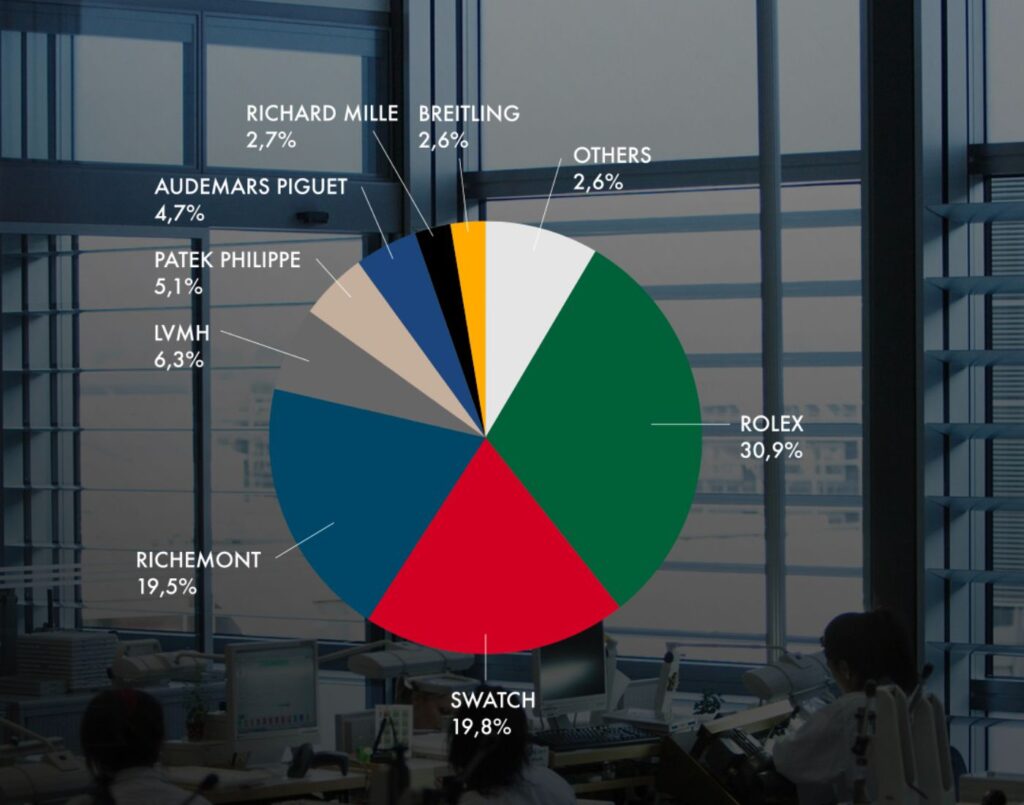

The export value of finished watches from the Swiss industry last year reached CHF 23.7 billion. This is up sharply from 2021 (+11.6 percent) but also compared to pre-pandemic levels in 2019 (+9 percent). As for retail sales, Morgan Stanley estimates the value to be around CHF 48 billion. Despite the increase in economic value, it is worth noting that there is no concomitant increase in volume. From 15.7 million watches exported in 2021, we have gone to just 15.8 million (+0.2 percent). This figure testifies even more clearly to the impact of price increases within the industry and also to a certain insensitivity of the target audience to the variant.  In terms of competition, the polarization trend we have witnessed has strengthened. Patek Philippe, Audemars Piguet, Richard Mille, and Rolex hold 41.7 percent market share (39.8 percent in 2021). The 4 big groups of the industry, Rolex, Swatch Group, Richemont and LVMH hold a stuggering 75% market share. An incredible figure to consider is that Rolex alone (not including Tudor), holds 29.2 percent of market share. Noteworthy, the year’s performance of Audemars Piguet, Breitling and Vacheron Constantin among the Bigs, but also Girard Perregaux and Ulysse Nardin, which consequently to the buy-out brought a result of +80% in sales over the previous year.

In terms of competition, the polarization trend we have witnessed has strengthened. Patek Philippe, Audemars Piguet, Richard Mille, and Rolex hold 41.7 percent market share (39.8 percent in 2021). The 4 big groups of the industry, Rolex, Swatch Group, Richemont and LVMH hold a stuggering 75% market share. An incredible figure to consider is that Rolex alone (not including Tudor), holds 29.2 percent of market share. Noteworthy, the year’s performance of Audemars Piguet, Breitling and Vacheron Constantin among the Bigs, but also Girard Perregaux and Ulysse Nardin, which consequently to the buy-out brought a result of +80% in sales over the previous year.

On the podium again this year we find Rolex, Cartier and Omega, in first, second and third positions respectively. Rolex remains firmly in the lead, even increasing its market share by 220 bps. As for Cartier and Omega, however, the situation is more complex. In fact, there is a real head-to-head between the brands. At the moment Cartier seems to be coming out on top in terms of sales, however Omega remains ahead of Cartier in terms of retail value and market share. This discord is most likely due to different management of retail/wholesale distribution channels. Immediately below the podium we find a pulse-pounding trio. Audemars Piguet in fourth, Patek Philippe in fifth, and Richard Mille in sixth. Audemars touches CHF 2 billion for the first time, unexpectedly consolidating its position against Patek Philippe. In seventh place, the last brand with sales above CHF 1 billion, is Longines. According to Morgan Stanley, the brand has lost as many as two positions in one year and 200 million euros in sales. The reason is, most likely, excessive exposure in the Chinese market, which is experiencing delays in the post-pandemic recovery. Thanks to the excellent performance of the last 3 years, IWC returns to the 8th position (Last time was 2017). Surprisingly, Breitling and Vacheron Constantin enters the top 10 in 9th and 10th position. The former has an impressive track record, gaining 10 positions in the last 6 years.

As we said, the industry is mainly in the hands of 4 major groups that together hold more than 75% of the market share by retail value. We are of course talking about Rolex, Swatch Group, Richemont and LVMH.

The leader again is Rolex, with 30.9 percent market share. This, too, is up from the previous year by as much as 1.5 percentage points. Although about 94 percent of sales can be attributed to the Rolex brand, Tudor also beat the industry in 2022 with sales of about CHF 550 million and an increase over 2021 of 11 percent. According to Morgan Stanley, the average selling price for Rolex is CHF 11,500, reflecting the fact that the largest volumes occur in its core collections in steel and steel and gold (Submariner, GMT, Explorer, Daytona). The brand strategy seems to be unchanged, a down-selling to Tudor for lack of Rolex products to increase brand desirability. Although waiting lists seem to have been reduced, they still remain largely prohibitive for many.

In second position with 19.8 percent market share, Swatch Group has lost a lot of ground this year. Compared to 2021, in fact, it is -2.2% and even -6.35% compared to 2019. Main driver of this result is, in all likelihood, the slowdown in the Chinese market. Suffice it to say that, according to Morgan Stanley, Omega and Longines are respectively the first and second brands in China by sales value. Morgan Stanley also estimates that by 2021, 70 percent of Longines’ sales would come from Chinese nationals worldwide. What impressed Swatch Group, on the other hand, was the performance of the Swatch brand, which thanks to the Moonswatch operation recorded an 87 percent increase in sales. In addition to high dependence on the Chinese market, Morgan Stanley also points to excessive internal polarization within the group. Indeed, of the 16 brands in the group’s portfolio, Omega, Longines, and Tissot occupy 59 percent weight in terms of sales value. Effectively, this is an important figure, but if we consider that in Richemont one brand – Cartier- holds almost 40 percent, then this statement turns out to be of little consequence in my opinion.

Richemont has experienced quite turbulent years but it seems that the worst is behind us. Market share remains stable at 19.5 percent. Overall, the group’s watch division brought in a result of CHF 3.8 billion, mainly fueled by the incredible performance of Cartier. In fact, the brand alone allows the group to gross 38.6 percent of total recorded sales and likely an even larger share of net earnings. Noteworthy for Richemont (in addition to Cartier), are the performances of Vacheron Constantin and IWC, very close to reaching CHF 1 billion in sales.

The LVMH group ranks fourth in the “Groups” ranking with market shares of 6.3 percent. Although it was not a particularly exciting year, all of the group’s brands maintained a positive trend. Among all of them certainly stands out Hublot, which overtook its Tag Heuer colleagues in terms of sales. In the ranking among others, a brand that has been absent until now makes its entry this year: Louis Vuitton. As we know, Arnault’s group in fact decided to focus heavily on the brand’s watch division, and the results seem to be indisputable. Morgan Stanley estimates a turnover for the division of 130 million CHF in 2022 and an average price of 3,724 CHF.

Leaving aside Audemars Piguet, Patek Philippe, and Richard Mille which we mentioned just above, it is very interesting to analyze the situation of other brands that do not belong to large groups.

Breitling is one of the best performing brands of the year. Over a period from 2017 to the present (the year the brand was bought by CVC), Breitling has gained 10 positions in the rankings to rank ninth in the top 10 by sales. In 2022 alone, sales value is estimated to increase by +27 percent. According to Morgan Stanley, this is the result of a number of factors: successful new launches and appropriate marketing initiatives, a reduced presence in China (but increasing year-on-year), and store rationalization with an increase in single-brand boutiques.

Hermès also records another impressive year. In fact, from 2018 to the present, the company’s watch division has grown at an impressive rate, from 2021 to 2022 alone, to CHF 519 million from about 364. The main merit is the company’s concentration on products that maintain the characteristic DNA of the aesthetically-conscious company, but without compromising on the quality of the purely mechanical and horological part. This commitment was also widely recognized this year by the jury of the Grand Prix D’Horlogerie, which awarded the brand two prizes.

Chopard’s performance has been up and down in the medium term. The brand continues to bounce between nineteenth and twentieth in the rankings by sales. Despite this, the company reported sales of CHF 410 million in 2022, up from CHF 369 million in 2021. In our opinion, given the success of the Alpine Eagle collection and the commitment to the company made in recent years, the results may be even better in the near future.

Although they are both part of the Sowind Group, we want to consider them as independent entities for this time, as they have recently come out of the sphere of influence of a truly large group: Kering. The management buy-out that took place a year ago seems to have been providential for the two brands, which have really struggled in recent years, but in 2022 experienced incredible growth of almost +50%. Follow us on Instagram not to miss any real-time update. Visit our Youtube channel to live the world of watchmaking firsthand.